Understanding cognitive biases in investment is crucial for personal development. Often, the state of your financial health limits the kind of life you can lead. Therefore, today this article will delve into the psychology of investment, sharing insights into healthy investment strategies and how psychological principles can help to build more robust investment habits.

Understanding cognitive biases in investment is crucial for personal development. Often, the state of your financial health limits the kind of life you can lead. Therefore, today this article will delve into the psychology of investment, sharing insights into healthy investment strategies and how psychological principles can help to build more robust investment habits.

Define Your Investment Goals

To excel in personal investment, it’s essential to consider your objectives.

Investment tools like cryptocurrencies, stocks, and bonds each have unique characteristics. Cryptocurrencies might offer quick, substantial returns but come with high risks. Bonds, on the other hand, offer lower returns with lower risks. High risk usually means high returns and low risk means low returns.

Understanding your long-term goals is crucial in selecting the right investment tools. For explosive wealth growth, high-risk investments might be suitable, but you must be ready to handle significant losses. Reflect on what you aim to achieve through investment, and then build your portfolio accordingly.

Suppose you are optimistic about a certain cryptocurrency and see its potential for appreciation, but its downside risk is also significant. If you can only accept a maximum of a 20% drop, you might need to set your stop-loss at 80% of your principal before buying that cryptocurrency.

Setting boundaries, such as stop-loss limits, is vital to manage risks. Recognising and overcoming cognitive biases will help you make more rational investment decisions about when to hold on or give up.

How to Manage Risks: Risk Hedging Strategy

When it comes to investment, risk hedging is a term that people frequently bring up, but what exactly is risk hedging though?

Risk Hedging means that the risks in your investment portfolio should complement the risks of your other financial sources. For example, if your primary income came from being the owner of a startup company, it would be relatively high risk and high reward. When things go well, your income can surpass many salaried workers, but issues can lead to financial losses.

So if the main income source is high-risk, creating a low-risk investment portfolio should be preferred.

Cognitive Bias 1: Gambler’s Fallacy

When creating an investment portfolio or making investment decisions, people encounter certain cognitive biases. The first cognitive bias is Gambler’s Fallacy, whichleads people to mistakenly believe that past patterns are necessarily related to future ones (Tversky & Kahneman, 1974). If you’ve ever been to a casino and played dice, you might have noticed a screen showing the results of the past ten rounds.

Some believe they can observe patterns in these results to predict whether the next outcome will be high or low. There are two ways to think about this: after ten consecutive highs, one might expect a low to follow, or alternatively, after ten highs, the trend might continue. Which one is correct? Both perspectives can seem logical because each outcome is independent of the previous ones.

In the stock market, a similar bias occurs. For example, in short-term technical analysis, if a stock’s price keeps rising, should it logically fall soon, or should it continue rising? The Random Walk Hypothesis suggests that stock prices follow a completely random path in the short term.

This is why investment ads often include a disclaimer: past performance is not indicative of future results. It is important to practise our critical thinking when investing,

Cognitive Bias 2: Confirmation Bias

Another important cognitive bias is confirmation Bias, in which individuals favour information that supports their preexisting beliefs and ignore evidence that contradicts them (Nickerson, 1998). In investment, this means that investors are likely to focus on data that confirms their strategy or belief while overlooking data that could indicate potential risks or alternative perspectives. This bias can lead to flawed decision-making, as it encourages the perception of order and predictability in random, unrelated data, distorting the reality of investment risks and opportunities. Even highly-intelligent people can fall into this trap.

Cognitive Bias 3: Conformity

Third, it’s important to understand the concept of conformity, a specific type of cognitive bias. People often exhibit a tendency to follow the crowd (Asch, 1951), such as in investment decisions. For instance, when you see your friends discussing a particular stock that’s rising quickly, you might feel compelled to invest in it, fearing that you’ll miss out if you don’t conform. This is a common manifestation of cognitive bias during bullish markets, where many inexperienced investors might appear successful.

However, blindly conforming to the crowd’s actions can be risky. Conformity as a cognitive bias means adhering to popular trends or opinions without critically assessing whether they align with your own financial goals or risk tolerance. This cognitive bias can lead to significant losses, as you might end up falling with the crowd if the market turns unfavourable. It’s crucial to be aware of this cognitive bias and ensure that your investment decisions are based on thorough analysis rather than just following others.

Understanding Conformity is also crucial. People often exhibit a tendency to follow the crowd (Asch, 1951), especially in investment decisions. For instance, when you see your friends discussing a particular stock that’s rising quickly, you might feel compelled to invest in it, fearing you’ll miss out if you don’t conform. This cognitive bias can lead to significant losses if the market turns unfavourable. It’s crucial to ensure your investment decisions are based on thorough analysis and wisdom rather than just following others.

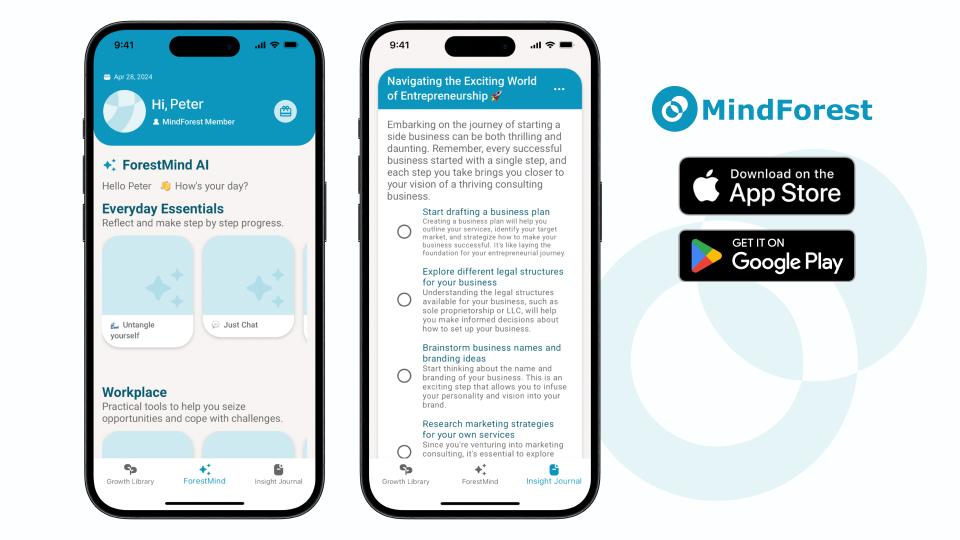

Download MindForest to Improve Investment Decisions and Avoid Cognitive Bias

Making sound investment decisions and avoiding cognitive biases are essential for financial success. MindForest helps you refine these skills:

1) Goal Setting and Tracking: Set investment goals and track progress. MindForest will prompt you to reassess strategies if they’re not meeting your objectives, helping you avoid biases that lead to poor decisions.

2) AI-Driven Scenario Analysis: Use AI coach ForestMind for practical simulations that challenge your decision-making, helping you recognise when to hold or cut losses and avoid biases like the sunk cost fallacy.

3) Reflective Insight Journal: AI-analyse your decisions with MindForest’s journal to spot and address cognitive biases. This feature encourages you to reevaluate unproductive investments.

Asch, S. E. (1951). Effects of group pressure upon the modification and distortion of judgments. In H. Guetzkow (Ed.), Groups, leadership and men; research in human relations (pp. 177–190). Carnegie Press.

Nickerson, R. S. (1998). Confirmation bias: A ubiquitous phenomenon in many guises. Review of General Psychology, 2(2), 175–220. https://doi.org/10.1037/1089-2680.2.2.175

Tversky, A., & Kahneman, D. (1974). Judgment under Uncertainty: Heuristics and Biases.Science (New York, N.Y.),185(4157), 1124–1131.

[@portabletext/react] Unknown block type "break", specify a component for it in the `components.types` prop

Want to understand yourself better? Download MindForest — a psychology-based AI self-discovery app to explore your inner world and manage emotions, anytime.

[@portabletext/react] Unknown block type "break", specify a component for it in the `components.types` prop

Psychology Insights & Life Applications

Discover practical psychology tips you can apply to your everyday life. From building resilience to improving relationships and finding work-life balance, our blog brings expert-backed insights that help you grow.

Age Gap in Dating: Does It Actually Matter? Here's What the Research Says - 5 Things to Consider Before Having a Relationship

So, You're Dating Someone Older (or Younger) — and People Have Opinions

Let's be honest. The moment someone finds out there is a notable age gap in your relationship, the questions start. "How old is he?" "Isn't that a bit weird?" "What do you two even have in common?" Whether you are 23 dating a 35-year-old, or 30 and seeing someone who is 42, you have probably felt the weight of other people's opinions before you have even had a chance to figure out how you feel yourself.

Here is the thing: age gap relationships are far more common than people make them sound, and the research on them is a lot more nuanced than your group chat might be. This article is here to give you the honest psychological picture — the real concerns, the genuine green flags, and the questions worth asking yourself before you let someone else's raised eyebrow become your own inner doubt.

5 Signs of Love Bombing: When Someone's "Perfect Partner" Energy Is Actually a Red Flag

Picture this. You match with someone, and within 48 hours they're texting you paragraphs. By week two, they're calling you their soulmate. By week three, they've already booked a couples' trip and introduced you to their mum. Your friends are screaming "run" whilst your brain is flooded with dopamine and your heart is doing something completely unhinged.

Here is the plot twist nobody tells you: that overwhelming, electric, "finally someone who gets me" feeling? It might not be romance. It might be love bombing — and once you know what to look for, you literally cannot unsee it.

This article breaks down exactly what love bombing is, why your brain falls for it every single time, and what to actually do if you think you're in the middle of it. No fluff. Just the honest, researched stuff you actually need.

Peter ChanManaging Director & Chief Psychology Specialist, TreeholeHK Limited

13 min read

Does AI Therapy Actually Work? Here's What Psychology Research Says

Can AI really help with mental health? We review the latest psychology research on AI therapy, from chatbot counselling to digital interventions — and what the evidence actually shows.

Ready to Apply Psychology to Your Life?

Download MindForest and turn these insights into action. Get personalized support from ForestMind AI Coach, track your progress, and unlock your full potential.